You’ve had the same financial argument fifteen times with your spouse, and each time you walk away frustrated because they “just don’t get it” while they’re equally frustrated because you “refuse to be reasonable.”

Beneath the surface, it’s apparent that the argument isn’t often about money itself. Rather, it’s about two different Wealth Dynamics profiles trying to make financial decisions using incompatible frameworks, and until you recognize this pattern, you’ll keep having the same conversation without resolution.

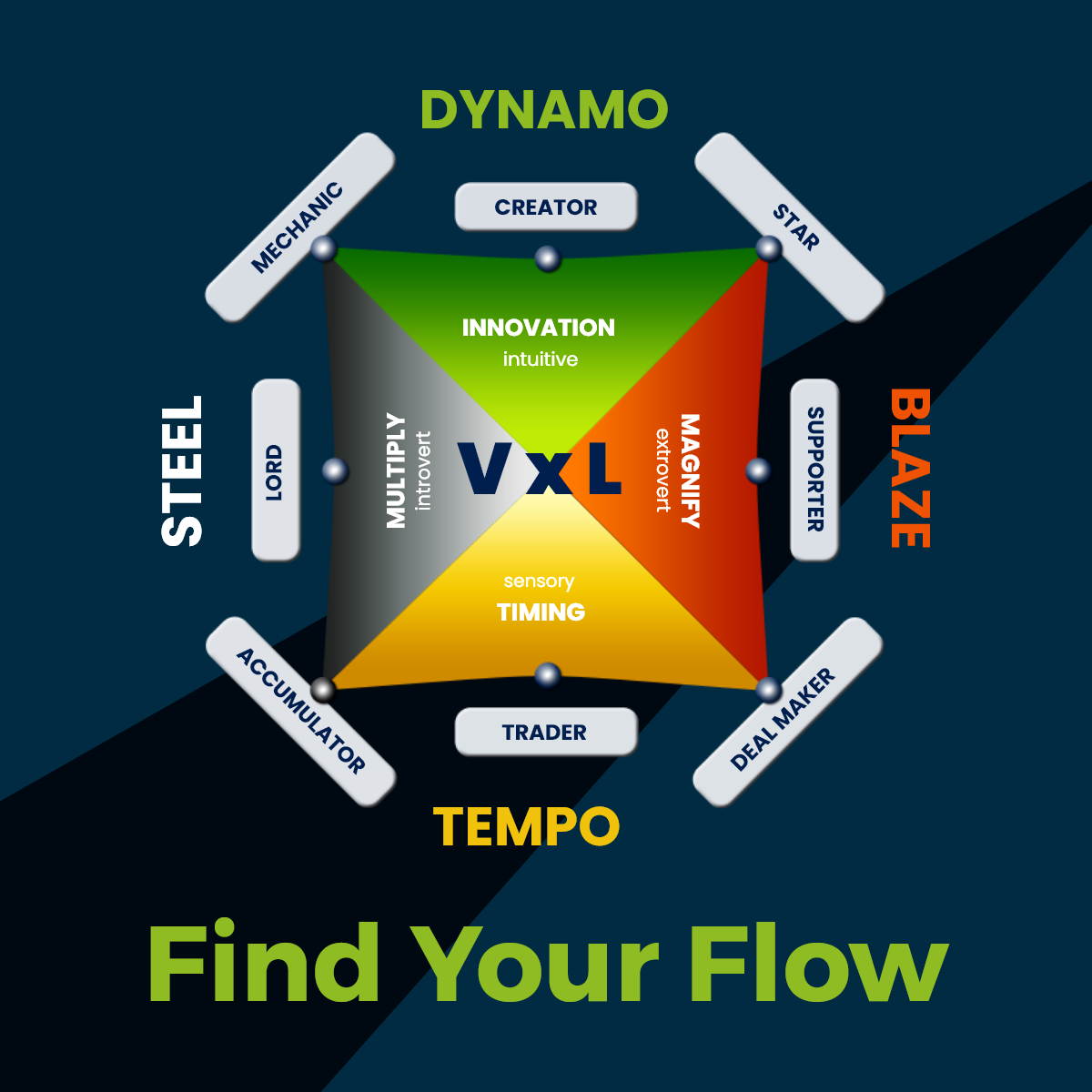

The Arguments That Reveal Your Profiles

“We should invest in this opportunity” vs. “We need to research this more.” One spouse sees timing and opportunity (Deal Maker or Trader thinking), while the other sees risk and insufficient information (Accumulator or Lord thinking). Neither is wrong, they’re evaluating through entirely different decision-making systems where one prioritizes speed and the other prioritizes certainty.

“Let’s reinvest profits to grow faster” vs. “Let’s secure what we have first.” Creator or Star profiles naturally want to expand and take calculated risks, while Mechanic or Accumulator profiles want to consolidate and protect gains. The growth-focused spouse feels held back by caution, while the security-focused spouse feels endangered by recklessness.

“I want to start this business” vs. “We need stable income right now.” Dynamo-spectrum profiles (Creator, Star, Supporter, Deal Maker) are energized by new ventures and possibilities, while Tempo-spectrum profiles (Trader, Accumulator, Lord, Mechanic) are energized by optimization and security. One sees opportunity cost in waiting, the other sees risk in moving too fast.

Why Your Money Values Clash

Different Wealth Dynamics profiles don’t just prefer different investment strategies, they have fundamentally different relationships with money, risk, and wealth building that create philosophical conflicts that feel personal but are actually structural.

Deal Makers see money as a tool for capturing opportunities and believe unused capital is wasted capital, becoming frustrated when their spouse wants to “sit on cash” instead of deploying it into deals. Accumulators see money as security requiring protection and become anxious when their spouse wants to “gamble” on opportunities without sufficient research.

Creators view investing in their next innovation as the highest-return use of money and resent being told to “get a real job” or “stop chasing ideas.” Mechanics view systematic business operations as the only sustainable wealth path and become frustrated when their spouse pursues unproven ventures instead of optimizing what’s already working.

Stars believe in investing in personal brand and relationship-building, seeing networking expenses and visibility investments as essential business costs. Traders see these as wasteful spending without measurable ROI and push for data-driven investment decisions.

The Framework That Actually Works

Stop trying to convince your spouse that your financial philosophy is objectively correct and start recognizing that both profiles have valid approaches that work for different people building wealth in different ways. Don’t try to convert them into accepting your perspective, but design financial structures that honor both profiles.

Create designated capital pools. Allocate percentages of household wealth to different strategies aligned with each spouse’s profile. Deal Maker spouse gets their opportunity fund, Accumulator spouse gets their security fund, and you stop fighting over every individual decision because the framework is pre-agreed.

Divide financial domains. Let each spouse lead in areas matching their natural strengths. Mechanic handles systematic investments and retirement accounts, Star handles relationship-based business development, and you leverage complementary strengths instead of forcing agreement on everything.

Set risk boundaries with agreed metrics. Define what percentage of net worth can go into speculative ventures, what must stay in secure assets, and what constitutes unacceptable risk. Numbers remove emotion from individual decisions once the framework exists.

Recognize that both of you are right. Your spouse’s conservative approach has prevented catastrophic losses you would have taken. Your aggressive approach has captured gains they would have missed. The optimal household financial strategy includes both perspectives rather than choosing one.

Once you recognize your money conflicts as profile differences rather than character flaws, conversations shift from “you’re being unreasonable” to “your profile needs security and mine needs growth, so how do we honor both?”

Discover your financial compatibility. Understanding both you and your spouse’s Wealth Dynamics profiles transforms money conflicts from personality clashes into strategic design challenges with clear solutions.